Are you scurrying around to find the right investment saving plan? Whether you’re an investor or not, the Unit Linked Insurance Plan (ULIP) might end up being the best choice for your investment requirements. This is because of ULIPs tax-saving quality and provision for higher returns.

Being a long term product, ULIP plan is one such tax saver that ensures a huge sum of money to safeguard all your dreams and aspirations. With its wealth-generating and risk-bearing ability, ULIPs are the right investment avenues that eventually manage your requirements. Keeping this in mind, we have listed down a few investments strategies in ULIP in order to help you maximize your gains:

List of Investment Strategies in ULIP for better returns

1. Automatic Transfer Strategy in ULIP

Automatic Transfer Strategy, popularly known as ATS is widely common among ULIP investments. Under ATS, you pay your premium initially in the debt fund and later, get a fixed amount transferred into your chosen equity fund.

Investing in an ATS will simply ensure that your premium will not be exposed to the stock market fluctuations. Another perk of using ATS is that it accumulates units at a lesser cost through rupee cost averaging.

2. Target Asset Allocation Strategy in ULIP

Do you know what plays an important role in deciding an investor’s portfolio? Well, the answer is none other than his asset allocation. Hence, see to it that you allot your premium into funds based on your appetite for risk and goals.

If you’re looking forward to implementing the target asset allocation strategy, then provide a mandate for allocation of premium in a fixed proportion between either equity funds or debt funds. Once you have allocated these funds, maintain this quarterly with rebalancing.

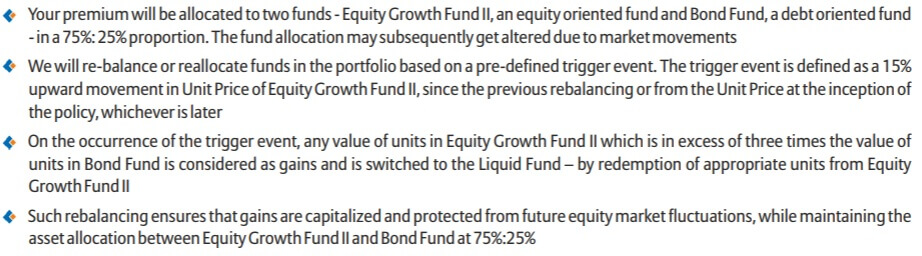

3. Trigger Portfolio Strategy in ULIP

If you’re the type of investor who believes in the strategy of ‘Buy low and sell high’, then the trigger portfolio strategy is perfect for you. Under this strategy, a policyholder is allowed to take advantage of substantial market swings.

In a trigger portfolio strategy, the premium is distributed amongst two funds – equity fund and income fund. Once the funds are allocated, you don’t need to keep continuous track of your ULIP performance. They’re auto-allocated based on a pre-defined trigger event. An example is shown in the image below

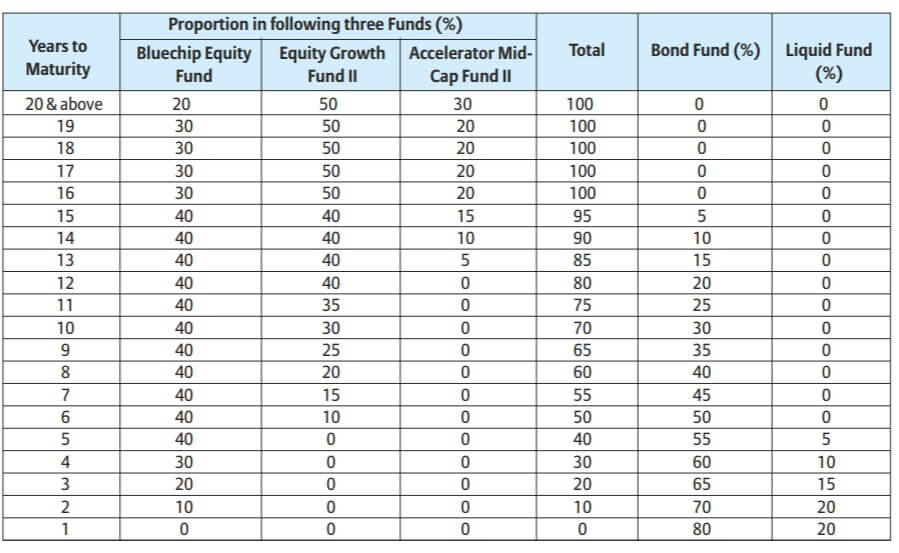

4. Age-Based Strategy in ULIP

Investing in an age-based strategy serves an investor with flexibility options. He can choose his funds based on his risk appetite. Employing an age-based strategy will let you start with aggressive risk appetite.

The age-based strategy will allow an investor to retire in peace. ULIP performance enhances the selection of an age-based strategy. An example is shown in the image below

5. Tax-free Withdrawals

Unlike mutual funds, you can effortlessly make withdrawals that offer tax-free savings. However, these withdrawals are possible only in special cases like the death of the policyholder, partial withdrawal at the discretion of the policyholder or maturity of the policy.

If a death benefit is paid under ULIP, then it is absolutely tax-free. Upon the date of maturity of ULIP, every policyholder receives the assured benefit or the value of the unit linked investments, whichever amount is higher.

So what are you waiting for? Explore Investing in ULIPs in order to benefit from its growth and protection aspects of the plan.