We must all suffer one of two things: the pain of discipline or the pain of regret or disappointment. – Jim Rohn. If you are looking for systematic and a well thought out plan that enables you to create long- term wealth and also protect yourself against the uncertainties of life, then you should consider Edelweiss Tokio Life WealthUltima. It is a systematic plan designed for accumulating your wealth by having an option to pay systematically through monthly or other modes, growing your wealth by capitalizing on multiple choices of STPs and/or funds and utilizing your wealth by opting for SWP. It would be a good investment for your retirement which can be enjoyed in grand style or it could be used to provide international education course for your child. This plan focuses on three important aspects Wealth Accumulation, Wealth Preservation, and Wealth Utilization. The article explains How do the Edelweiss Tokio Life WealthUltima works?

How do the Edelweiss Tokio Life WealthUltima works?

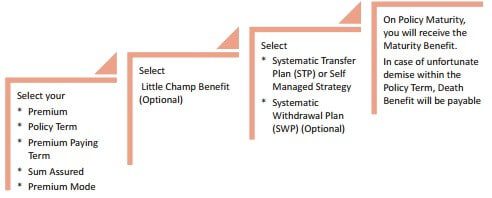

- You need to choose Policy Term and Premium Paying Term as per your need: Policy Term ranges from 10 years to ‘till age 100’. Premium Paying Term(PPT) ranges from 5 years to ‘till the end of the policy term’.

- It provides life cover which gives a lump sum amount to the beneficiary in case of unfortunate demise of the Life Insured.

- It provides Little Champ Benefit where in the case of unfortunate demise of the Policyholder, the policy shall continue and the child receives the Policy benefits as planned.

- Tax Benefits: You can avail income tax benefits on the premiums paid and on the benefits received as per the prevailing income tax laws.

- Additions in the Policy: This plan has 3 types of additions in the fund which enhance your fund value and reduce the total cost:

- Loyalty Additions: Rewards you for continuously paying your premiums. Ex Loyalty Addition will be 0.15% of average of daily Fund Value of last 12 month starting from the end of sixth Policy Year till the end of the Premium Paying Term, provided all the Premiums which have fallen due for that Policy Year have been paid

- Guaranteed Additions: Rewards you for staying invested. Guaranteed Additions will be added to the Fund Value at the end of every Policy Year, starting from the end of sixth Policy Year till the Maturity Date of the policy.

- Booster Additions: Ensures effective growth of your fund value. Booster Additions will be added to the Fund Value at the end of every fifth Policy Year starting from end of 10th Policy Year till the Maturity Date of the Policy and is around 2.75-3.5% depending on tenure of the policy Systematic Monthly Plan (SMP): Under SMP, you pay your premium on a monthly basis. This helps as it is Easier to pay a small amount monthly than a large amount annually and it helps in Safeguarding from erratic market movements

- Systematic Transfer Plan (STP): It is often difficult to ascertain which asset class to choose and when to switch between them. STP offers two options set out below to help manage your asset allocation as per your needs:

- Lifestage and duration based STP: This STP ensures your money is moved from equity oriented fund (Equity Large Cap Fund) to debt oriented fund (Bond Fund) as your age increases and remaining policy term reduces. The allocation percentage in Equity Large Cap Fund will be equal to (100-attained age) multiplied by remaining Policy Term divided by 10. This allocation percentage cannot be more than 100%. Remaining fund value will be allocated in Bond Fund

- Profit target based STP: This STP enables you to lock the gains made from equity and reduce the future market volatility by transferring the gains to a safer avenue. Under this STP, 100% of the Premiums (net of allocation charges) are invested in Equity Large Cap Fund. On any day where the gain from the gain in the Equity Large Cap Fund reaches 10% or more of the cumulative premiums (including Top-up premiums) paid, the entire amount equal to the appreciation will then be transferred to the Bond Fund at the prevailing unit price.

- You can also choose the Self-Managed Strategy wherein your money will be allocated to your choice of the fund(s).

- Systematic Withdrawal Plan (SWP): This option allows you to withdraw a sum of money systematically and regularly from your Fund Value. This regular stream of money works as a second income for you. On survival of the Life Insured, at the end of the Policy Term, and provided the Policy is In-force, Fund Value will be paid as Maturity Benefit. However, you have the option to collect the maturity proceeds in instalments. This option is called Settlement Option.

- Settlement Option: Under this option, the amount paid out in each instalment will be the outstanding Fund Value as on that instalment date divided by the number of outstanding instalments. Under this option, you need to choose:

- Settlement Term (option of 1, 2, 3, 4 or 5 years); and

- Frequency of payout (yearly, half-yearly, quarterly or monthly instalments)

- For example, you choose the Settlement Term of 3 years to be paid out in monthly instalments which means you have opted for 36 instalments.

- Let’s say the fund value at the beginning of Settlement Option period is Rs. 50,00,000. The first payout will be Rs. 50,00,000 / 36 = Rs. 1,38,889.

- Let’s say at the time of 15th instalment, the fund value is Rs. 33,50,000. Here, outstanding instalments are now 22. Hence, the 15th payout will be calculated as Rs. 33,50,000 / 22 = Rs. 1,52,273

- Note: It is New Age Unit Linked Insurance Plan or ULIP. The Linked Insurance Products do not offer any liquidity during the first five years of the contract. The policyholder will not be able to surrender/withdraw the monies invested in Linked Insurance Products completely or partially till the end of the fifth year.

“When you engage in systematic, purposeful action, using and stretching your abilities to the maximum, you cannot help but feel positive and confident about yourself”. For more information about the plan Edelweiss Tokio Life – WealthUltima