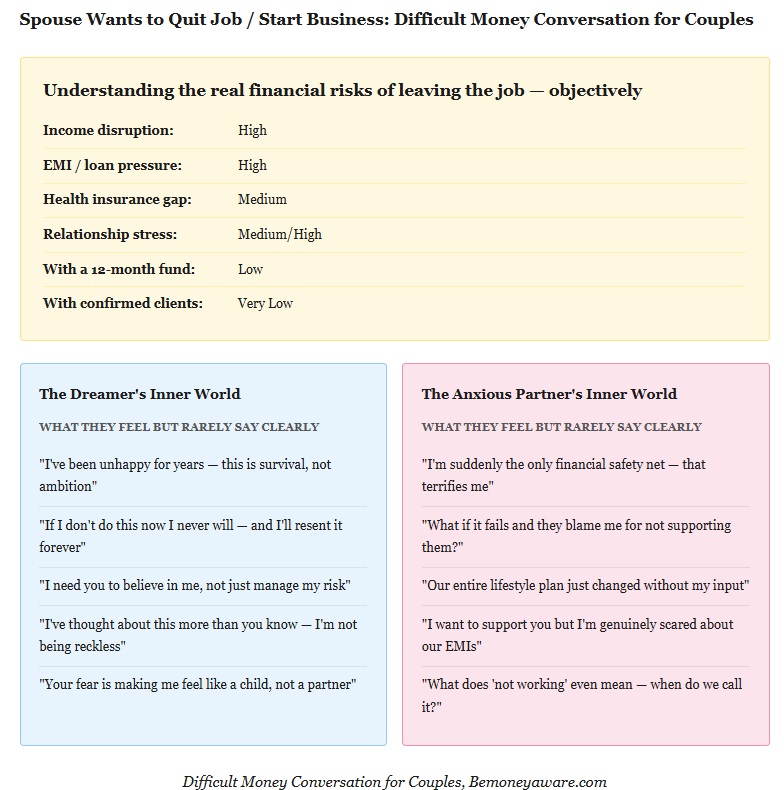

When a partner wants to quit job to start a business, it triggers one of the most emotionally charged money conversations a couple can have. India now has more first-generation entrepreneurs — yet the cultural narrative around job security, family obligation, and the shame of failure makes this one of the most emotionally charged conversations a couple can have. The partner who wants to leap is fighting years of “government job is safest” conditioning. The partner who is afraid is not being unsupportive — they are being rational. Both deserve to be heard. Neither should be dismissed.

Table of Contents

Financial Risks When Your Partner wants to Quit Job to Start a Businesss

What NOT to Say when your Partner wants to quit Job to start business

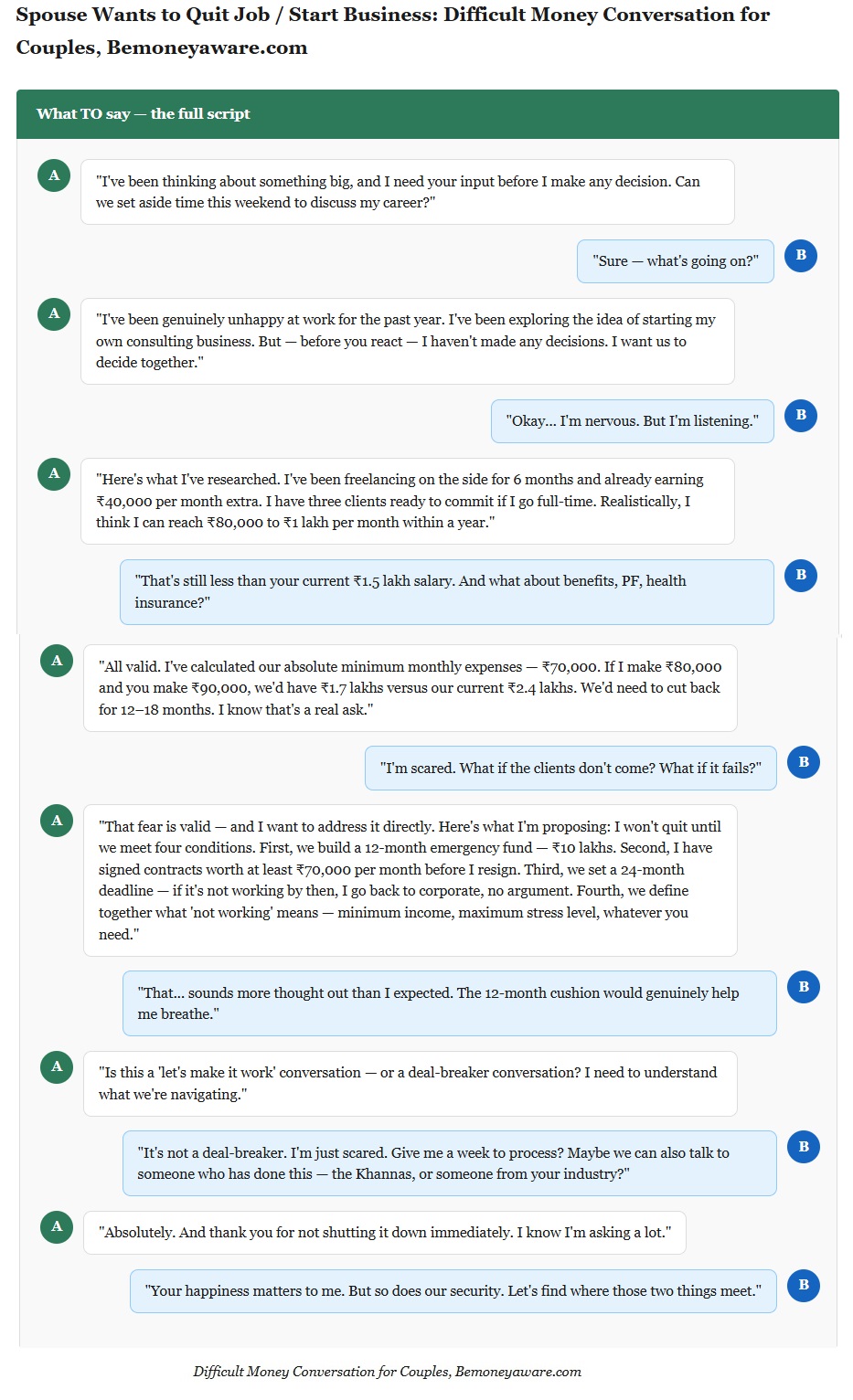

A: “I’m quitting my job next month to start my own business. I’ve made up my mind.”

B: “What?! You can’t just decide that! What about our home loan EMI? What about our security?!”

A: “You never support my dreams! You just want me to be miserable in corporate forever!”

B: “And you never think about us — only about yourself!”

What TO Say when your Partner wants to quit Job to start business

The 4-Step Framework

- Invite — Bring them in before you decide, not after. Present an idea, not a decision.

- Prove — Show evidence, not just enthusiasm. Side income earned, clients interested, market research done.

- Address — Answer the fear with a safety plan. Emergency fund, income threshold, health insurance, exit timeline.

- Define — Agree on what failure looks like before you start. Pre-agreed answers prevent goalpost creep.

The 4 Non-Negotiable Safety Conditions

- 12-Month Emergency Fund (₹10L+) — Built before resignation. Covers EMIs, living expenses, and health costs without pressure on every slow month.

- Signed Client Contracts (₹70K+/month) — Before the last day at work. Not “pipeline” — signed agreements covering at least 50% of target income.

- Health Insurance — Active from Day 1 — Employer cover ends on last working day. Individual or family floater must be purchased before resignation.

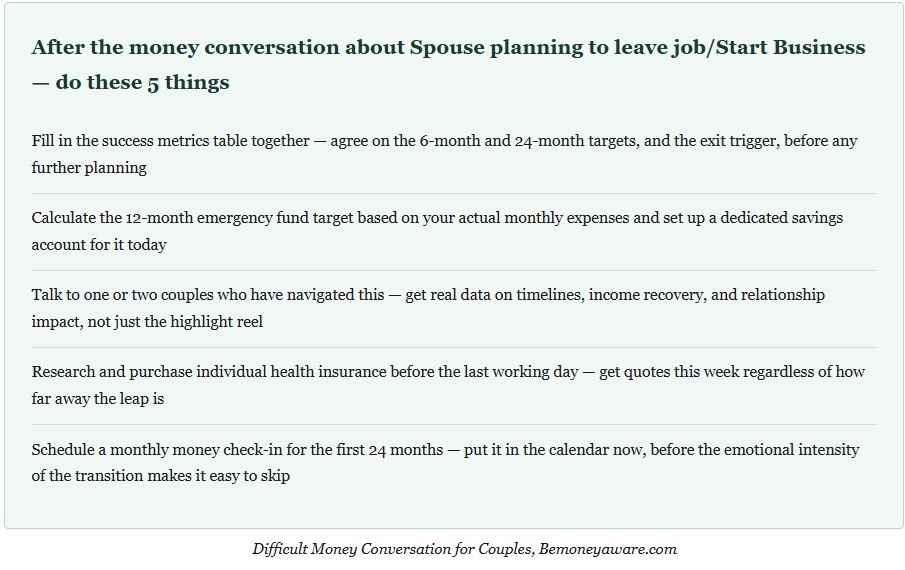

- Pre-Agreed Exit Criteria (24-month max runway) — Both partners define in writing: income trigger for return to employment, timeline, and what success looks like at 6, 12, and 24 months.

Define Success Together — Before Day One

| Metric | Month 6 Target | Month 24 Target |

|---|---|---|

| Monthly revenue | ₹60,000 | ₹1,20,000 |

| Number of active clients | 3 clients | 6–8 clients |

| Emergency fund remaining | ₹7L minimum | Replenished |

| Stress level (1–10 scale) | Below 7 | Below 6 |

| Relationship check-in rating | Monthly review | Quarterly review |

| Exit trigger — income below | ₹40,000 for 3 months | Return to employment |

The Smart Transition — 4 Phases

Phase 1 · Months 1–3 — Validate Without Quitting

Start as a side project while still employed. Get first paying clients. Generate real revenue data, not projections.

Target: First ₹20,000–40,000 in side income from real clients

Phase 2 · Months 4–9 — Build the Safety Net

Build the emergency fund to 12 months of expenses while side income grows. Both partners cut discretionary spending.

Target: ₹10L emergency fund + ₹70,000/month in confirmed side contracts

Phase 3 · The Leap — Resign With Conditions Met

This is the moment every couple faces when a partner quits job to start business — the leap is only safe when all four conditions are already met. Submit the resignation only then.

Buy health insurance on day one.

Set up weekly tracking visible to both partners.

Target: Both partners sign off on the metrics table and exit criteria before the letter goes in

Phase 4 · Months 1–24 Post-Leap — Build Openly

Monthly check-ins on agreed metrics — no blame, just data. Celebrate every milestone. If metrics are missed for three consecutive months, activate the exit plan without ego.

Target: Weekly money minute + monthly formal review for the full 24-month runway

When to Activate the Exit Plan

- Income stays below the agreed minimum for three consecutive months with no reversal in sight

- Emergency fund drops below 3 months of expenses with no recovery plan

- Relationship stress stays above the agreed threshold for two consecutive monthly check-ins

- The 24-month runway ends without reaching agreed targets

- A health or family emergency depletes the emergency fund below the safety threshold

- Both partners formally agree, during a calm review, that the experiment is not working

What Partner wants to Quit Job to Start Business? 3 Ways the Anxious Partner Can Support

- The Stability Partner

- Maintain your income, manage shared expenses, and be the emotional anchor during turbulent months. Your stability is an active contribution, not a passive background role.

- The Thinking Partner

- Engage with the business — ask questions, review the numbers, give honest feedback. Your outside perspective is often the most valuable asset a first-time founder has.

- The Celebration Partner

- Notice and name every milestone — first client, first ₹50K month, first referral. Entrepreneurship is lonely. Your recognition of progress is fuel no market success can replace.

Have This Conversation the Right Way

Download the free Money Dates Guide — it includes a full guided conversation with the safety plan template, metrics worksheet, and exit criteria framework built for Indian couples.

Take the Money Compatibility Quiz

Download the Free Money Dates Guide

Instagram Channel for Income Tax

Next: Episode 7 — Dealing With Wedding or Festival Debt Together

All Episodes in This Series

- When Your Partner OverSpends

- When Supporting Parents Is Straining Your Marriage

- When You Discover Secret Debt or Hidden Spending

- When You Disagree on When to Have Children

- When One of You Earns Significantly More

- When One Partner Wants to Quit and Start a Business ← You are here

- Dealing With Wedding or Festival Debt Together

What money conversation have you been avoiding?

Share this article with your partner as a starting point — sometimes the easiest way to open the conversation is to read something together.