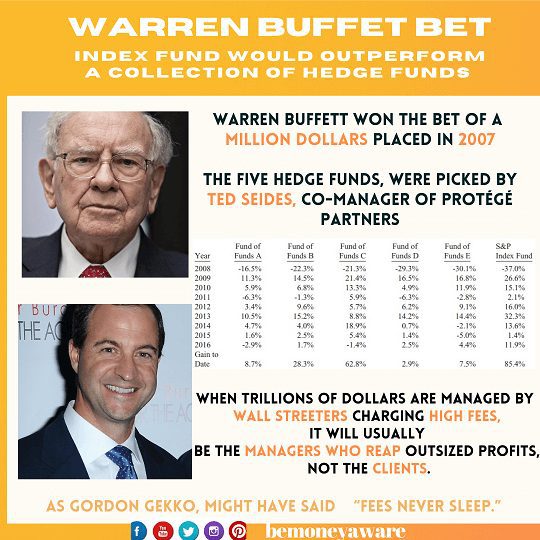

Warren Buffet won the bet of a million dollars that he had placed in 2007. The bet was that an index fund would outperform a collection of hedge funds over the course of 10 years. He said that by investing in a boring, low-cost stock index fund you could outperform most hedge funds. His pick, the S&P 500 (OEX), gained 125.8% over ten years. The five hedge funds, picked by a Ted Seides co-manager of Protégé Partners, added an average of about 36%. Not only did the investors in these hedge funds receive subpar returns, but they also paid an enormous amount in fees for that privilege. In this article, we shall look in detail at the Warren Buffet bet in detail, how do fees such as expense ratio affect the gains from Mutual Funds

Join our Telegram Group BeMoneyAware and Checkout our Instagram Channel Bemoneyaware

Costs really matter in investments,” Buffett says. “If returns are going to be 7 or 8 percent and you’re paying 1 percent for fees, that makes an enormous difference in how much money you’re going to have in retirement.

Table of Contents

The Warren Buffett bet with Hedge Fund Manager

In Berkshire’s letter of2016 on Page 21, Warren Buffet talked about “The Bet” (or how your money finds its way to Wall Street).

In Berkshire’s 2005 annual report, I argued that active investment management by professionals – in aggregate – would over a period of years underperform the returns achieved by rank amateurs who simply sat still.

Buffett’s contention was that an S&P 500 index fund would outperform a hand-picked portfolio of hedge funds over 10 years, due to fees, costs, and expenses, So basically The bet pit two basic investing philosophies against each other: passive and active investing.

Ted Seides co-manager of Protégé Partners, an asset manager that had raised money from limited partners to form a fund-of-funds, stepped up to challenge.

The bet officially commenced on January 1st, 2008. The names of the funds were not disclosed.

The prize money was invested in zero-coupon Treasury bonds(the sides initially put $640,000 (split evenly)) that were structured to rise to $1 million over 10 years. But the financial crisis saw interest rates plunge and sent the bonds up to nearly $1 million in 2012. By mutual agreement, the bettors sold the bonds and bought (actively managed) Berkshire B-shares, which were worth $1.4 million as of mid-February 2015.

The Protégé co-founder, who left in the fund in 2015, conceded defeat ahead of the contest’s scheduled wrap-up on December 31, 2017, writing, “for all intents and purposes, the game is over. I lost.”

As decided in the original bet, the money went to charity. Buffett’s charity pick was Girls Inc., an organization that supports young girls in Omaha through after-school and summer programs.

Warren Buffet even went ahead to say that If a statue is ever erected to honor the person who has done the most for American investors, the handsdown choice should be Jack Bogle. For decades, Jack has urged investors to invest in ultra-low-cost index funds.

Many feel that, If the period running from the beginning of 2008 through 2017 had seen a second swoon, Protégé’s co-founder might be writing sassy declarations of victory rather than what about it. While this battle has been won, the active-passive war will rage on.

Excerpts from Warren Buffett’s 2016 Berkshires letter are given below.

In this section, you will encounter, early on, the story of an investment bet I made nine years ago and, next, some strong opinions I have about investing

In Berkshire’s 2005 annual report, I argued that active investment management by professionals – in aggregate – would over a period of years underperform the returns achieved by rank amateurs who simply sat still. I explained that the massive fees levied by a variety of “helpers” would leave their clients – again in aggregate – worse off than if the amateurs simply invested in an unmanaged low-cost index fund.

Subsequently, I publicly offered to wager $500,000 that no investment pro could select a set of at least five hedge funds – wildly-popular and high-fee investing vehicles – that would over an extended period match the performance of an unmanaged S&P-500 index fund charging only token fees. I suggested a ten-year bet and named a low-cost Vanguard S&P fund as my contender. I then sat back and waited expectantly for a parade of fund managers – who could include their own fund as one of the five – to come forth and defend their occupation. After all, these managers urged others to bet billions on their abilities. Why should they fear putting a little of their own money on the line?

What followed was the sound of silence. Though there are thousands of professional investment managers who have amassed staggering fortunes by touting their stock-selecting prowess, only one man – Ted Seides – stepped up to my challenge. Ted was a co-manager of Protégé Partners, an asset manager that had raised money from limited partners to form a fund-of-funds – in other words, a fund that invests in multiple hedge fund

For Protégé Partners’ side of our ten-year bet, Ted picked five funds-of-funds whose results were to be averaged and compared against my Vanguard S&P index fund. The five he selected had invested their money in more than 100 hedge funds, which meant that the overall performance of the funds-of-funds would not be distorted by the good or poor results of a single manager. Each fund-of-funds, of course, operated with a layer of fees that sat above the fees charged by the hedge funds in which it had invested. In this doubling-up arrangement, the larger fees were levied by the underlying

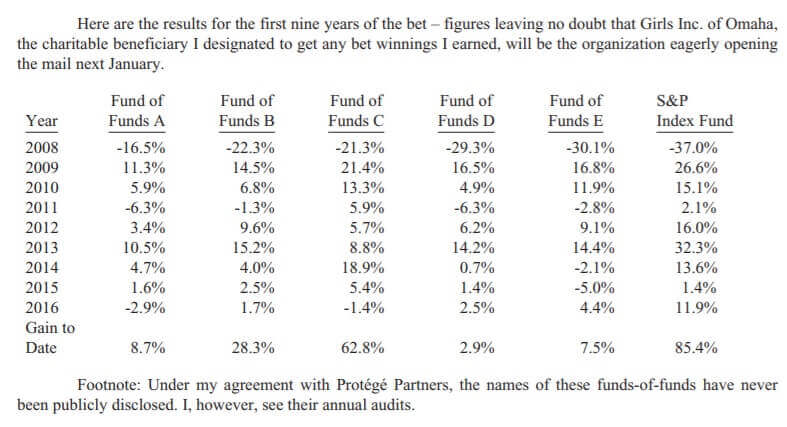

The hedge funds; each of the fund-of-funds imposed an additional fee for its presumed skills in selecting hedge-fund managers. Here are the results for the first nine years of the bet – figures leaving no doubt that Girls Inc. of Omaha, the charitable beneficiary I designated to get any bet winnings I earned, will be the organization eagerly opening the mail next January.

If a statue is ever erected to honor the person who has done the most for American investors, the hands-down choice should be Jack Bogle. For decades, Jack has urged investors to invest in ultra-low-cost index funds. In his crusade, he amassed only a tiny percentage of the wealth that has typically flowed to managers who have promised their investors large rewards while delivering them nothing – or, as in our bet, less than nothing – of added value.

In his early years, Jack was frequently mocked by the investment-management industry. Today, however, he has the satisfaction of knowing that he helped millions of investors realize far better returns on their savings than they otherwise would have earned. He is a hero to them and to me.

Costs associated with Active Investing

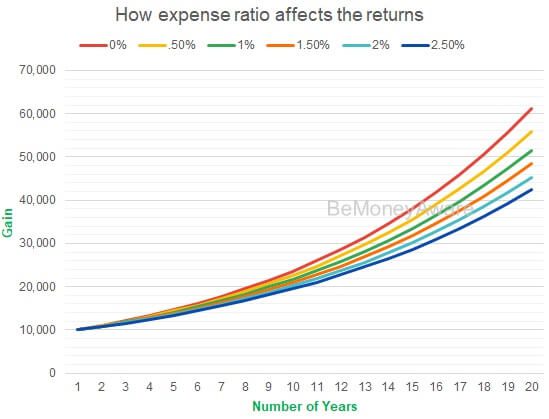

An expense ratio of 1% may not sound like a lot of money, but over the course of 30 years, it could take away a significant chunk of your earnings.

For example, if you invest Rs.50,000 in a fund with an expense ratio of 2%, then you are paying the fund house Rs.1,000 to manage your money. It can be said that if a fund earns 10% and has a 2% TER, then it means an 8% return for an investor. The mutual fund’s NAVs are reported after netting off the fees and expenses, and hence, it is necessary to know how much the fund is deducting or charging as expenses

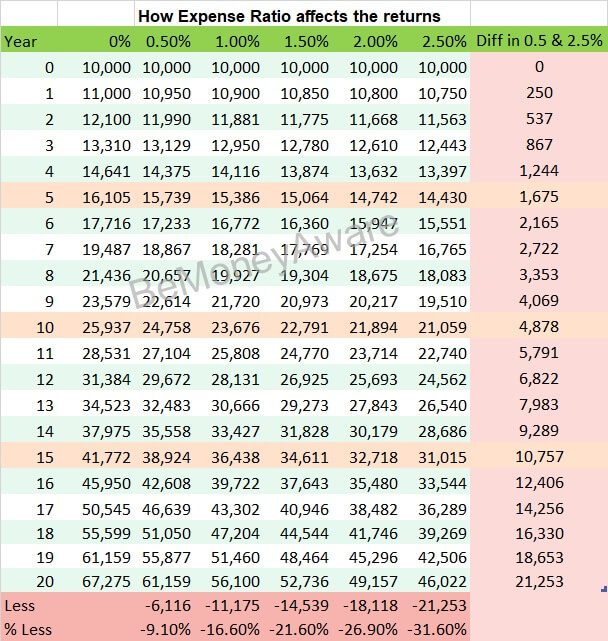

To see how expense ratios can affect your investments over time, let’s compare the returns of several hypothetical investments that differ only in expense ratio. The following table depicts the returns on a $10,000 initial investment, assuming an average annualized gain of 10%, with different expense ratios (0.5%, 1%, 1.5%, 2%, and 2.5%)

Excerpts from Warren Buffett’s 2016 Berkshires letter regarding costs are also given below.

When trillions of dollars are managed by Wall Streeters charging high fees, it will usually be the managers who reap outsized profits, not the clients. Both large and small investors should stick with low-cost index funds

How expense ratio affects the returns from Mutual Funds in tabular format

Warren Buffett on Cost of Funds

Excerpts from Warren Buffett’s 2016 Berkshires letter regarding costs are also given below.

The underlying hedge-fund managers in our bet received payments from their limited partners that likely averaged a bit under the prevailing hedge-fund standard of “2 and 20,” meaning a 2% annual fixed fee, payable even when losses are huge, and 20% of profits with no clawback (if good years were followed by bad ones). Under this lopsided arrangement, a hedge fund operator’s ability to simply pile up assets under management has made many of these managers extraordinarily rich, even as their investments have performed poorly.

Still, we’re not through with fees. Remember, there were the fund-of-funds managers to be fed as well. These managers received an additional fixed amount that was usually set at 1% of assets. Then, despite the terrible overall record of the five funds-of-funds, some experienced a few good years and collected “performance” fees. Consequently, I estimate that over the nine-year period roughly 60% – gulp! – of all gains achieved by the five funds-of-funds were diverted to the two levels of managers. That was their misbegotten reward for accomplishing something far short of what their many hundreds of limited partners could have effortlessly – and with virtually no cost – achieved on their own.

What other investors say about investing in Index Funds

If you don’t know too much about markets, the best way to invest your money right now is to put it in a cheap S&P 500 SPX fund, says Mark Cuban of Shark Tank, in his interview with Hayman Capital Management founder Kyle Bass

“Index funds take a ‘passive’ approach that eliminates almost all trading activity. When you own an index fund, you’re also protected against all the downright dumb, mildly misguided or merely unlucky decisions that active fund managers are liable to make” Tony Robbins writes in his book, Unshakeable

Lessons Learnt from the Warren Buffet Bet

- It is extremely tough to outperform the market. You may have a fairly decent chance to outperform it during the bear market, but during the bull run, you will miss on lots of gains by continually going in and out of your positions.

- High trading activity diminishes returns. The main reason is obviously the trading fees. Each time you make a trade, you pay trading fees and this has an additional negative impact on your portfolio. In addition to this, the more you trade, the more mistakes you can (and will) make.

- Passive investing is the best choice for the vast majority of investors. By being a passive investor, you will outperform 99.99% of other market participants, including the brightest minds at the world’s top hedge funds.

Aesop’s tale of tortoise and hare

It reminds us of Aesop’s tale of tortoise and hare.

While the active investor, the hares, bound around between exotic asset classes and elaborate derivatives, charging high fees for their troubles, worry about other things while the market, passive index investors, the tortoises, keeping significant short-term turbulence aside, gradually gains in value.

Join our Telegram Group BeMoneyAware and Checkout our Instagram Channel Bemoneyaware

Related Articles:

- Best Index Mutual Funds and ETF for 2021: Passive Investing

- What is ETF, Difference between ETF and Mutual Fund, ETF vs Index Fund, How to buy or sell ETF

- How to choose a stockbroker? Where to open a Demat Account?

- Does Index Fund or ETF Work? Will it work in India

- International Mutual Funds: What are these, Pros and Cons, Tax

As Gordon Gekko, a character in the 1987 film Wall Street and its 2010 sequel Wall Street: Money Never Sleeps, instead of Money never sleeps might have said “Fees never sleep.”

What do you think of the Warren Buffett bet? Do you think Warren Buffet was lucky to win the bet? Do you believe Index Funds or ETFs are better than Regular Mutual Funds? Do you invest in Index Fund?