While a portion of the Rs. 41 lakh bill for the late playback singer’s hospitalisation has already been paid by the family, Manna Dey’s daughter Shumita said the rest would be paid soon. “We have paid Rs. 16 lakh towards the bill and we hope to clear the dues in some time. The hospital has given us time to pay the rest,” she said. Manna Dey passed away on 24 Oct at at the Narayana Hrudayalaya Hospital in Bangalore where he was admitted with respiratory problems in May and was treated for the five months. Manna Dey’s family made a representation to the chief minister of Karnataka about financial assistance to the family in clearing his medical bills. In the letter, the family stated that when they left the hospital to take Dey’s body for the last rites, they were not able to clear all the pending bills.

When Manna Dey passed away in Oct 2013 at the age of 94, newspapers, internet were full of the life,music,songs of Manna Dey. While reading about him the above news caught my eyes. It made me think a person passing away leaves a void for his family members but at-times also huge medical bills to pay. How could one avoid such a situation? But then illness has no age limit. What if young person has severe illness, how will the family afford the medical expense? Medical care is advancing but health care costs are also increasing. So how does one prepare for rising medical costs? Health insurance is one of the solution. The purpose of health insurance is to protect you and your family financially in the event of an unexpected illness or injury that could be very expensive. It makes lot of sense to have health insurance but still many of us don’t have health insurance. Why?

Overview of Health Insurance

Health insurance is type of insurance that pays for medical and surgical expenses that are incurred by the insured. The type and amount of health care costs that will be covered by the health plan are specified in advance. Health plans are available in various formats :

- Individual Plan: In an individual policy you are personally the owner of the policy.

- Family Floater Plan : It is similar to individual health plans i.e one owns the policy but it is extended to cover your entire family. It enables the family members to claim access to a larger shared pool, than individual covers, considering the low probability of the entire family getting hospitalised in a single year

- Group plans :In a group plan, the sponsor owns the policy and the people covered under it are called its members.

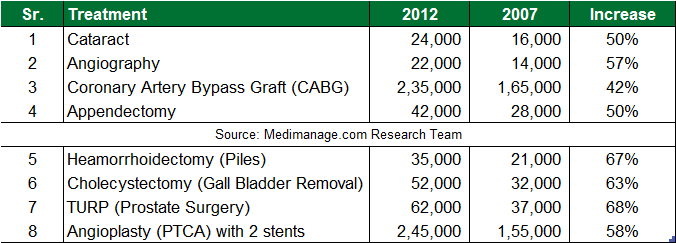

There are other variations are Critical Illness Policy, Senior Citizen policy, Student Medical insurance and Overseas Mediclaim Policy. Typically Individual or FamilyPolicy excludes any pre-existing ailments typically for the first four-five years. Other than this, insurance policies have waiting period clause for some specified illnesses. Costs of medical treatment are going up and up. Here are the 2012 costs for surgeries, compared with costs in 2007 from mediamanage

To get idea of kind of policies for health insurance in India offered one can check website of health insurers such as Royal Sundaram health insurance polices

Why we don’t buy health insurance?

I am Young and healthy

I am young and healthy and therefore I will not contract any major illness. Even if I am hospitalized, I can handle the bills myself. Most people do not believe in buying a health insurance when they are in good health. When you are healthy and rarely see a doctor, it may seem like a good idea to cut out health insurance and hence young people refrain from buying a health insurance policy. They feel it needs to be taken only when they grow older as they do not need insurance in their prime. When you are in a good health buying a health insurance policy ensures that you have a comprehensive cover when you are young and even when you choose to retire. When you buy a health insurance when you are in good health, you can also enjoy the benefits of cumulative bonus or discounts on premiums, if you continuously renew the policy without any claims. But are the young really healthy? I read the article Stroke strikes the young and active too, Times of India(Bangalore) on 30th Oct, which had some disturbing numbers on strokes.

- Strokes are increasingly affecting young and middle-aged people

- More than 83,000 people below 20 years affected each year globally

- Stroke-induced deaths in India have shot up from 1.3 lakh a year in 1990 to 2.63 lakh a year in 2010.

So young age is no protection against illness. What if one meets with an accident? Who pays for the hospital bills?

Corporate Health Insurance

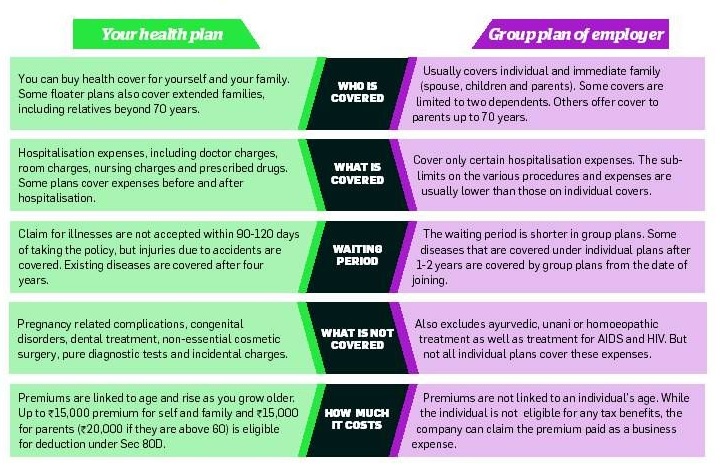

Most employees in the organized segment depend on the employer for health insurance which is typically Group health insurance. This perk is provided by company to all its employees’ across the board and not taken to suit individual’s need. Thanks to the global economic turmoil, companies are in the cost-cutting mode. Increase in the cost of group health insurance has made many employers rethink the benefit they provide through group health insurance. For example many companies are excluding employer’s parents from group health insurance. If it is your case then you need to purchase separate health insurance for your parents or if you have more than one claim in one year and you exceed your cover amount of corporate health insurance policy, you would have to pay the residual amount. So a corporate health insurance is not a complete solution. Comparison of individual and Corporate health plan is given below (Ref: ET Wealth)

Also if you happen to loose your job or you are between jobs then you are without any health insurance. God forbid if something happens then? Once you retire, employer provided group health insurance also retires. After retirement, someone who has worked for a company for majority of his life will find that the company health insurance which had taken care of all the medical bills is no longer available. If one has to purchase new health insurance after retirement the premium rates will be high as premium has a direct co-relation with the age of the policyholder. Then insurance companies also have waiting period of 24 to 48 month on pre-existing diseases. Will you be able to afford it that time? Will you be able serve the waiting period?

Getting claims settled is difficult

Some of us have think that claims of a health insurance policy are always rejected or one has to go from pillar to post to get them settled. In Cashless settlement, if the treatment is in a network hospital of the insurance provider the insurance company pays the hospital directly through their Third Party Administrator. In the Reimbursement settlement one pays then files a claim for reimbursement with the health insurance company’s. If you have the right documents with you, your claim should get approved. The claims settling ability of an insurer becomes important.Unfortunately, this data is still not ready in a handy and comparable format. Livemint’s Will your health cover finally pay up? has tried to mine the data. On high rejection ratio it says

One of the main reasons for a high rejection ratio, according to insurers, is claims made on account of pre-existing ailments and other initial-period policy exclusions. Health insurance excludes any pre-existing ailments typically for the first four years. Other than this, insurance policies have waiting period clause for some specified illnesses. So if a policyholder makes a claim on these accounts during the waiting period, the insurance company will be constrained to deny the claim.

The regulator defines a pre-existing ailment as any condition, ailment or injury or related conditions for which the policyholder had signs or symptoms, and/or were diagnosed, and/or received medical advice/treatment within 48 months prior to the first policy issued by the insurer.But what if policyholder has symptoms of a pre-existing disease but is aware that they have contracted the disease or the symptoms are silent.

Related Articles :

[poll id=”53″]

The healthcare costs are rising. Diseases and accidents do not come with warning and if they require unexpected hospitalization then is not just a major threat to your health but your savings as well. It makes me wonder Are we suffering from a serious medical condition called no health insurance? Shouldn’t we be prepared then repent later.

6 responses to “Why don’t we buy Health Insurance Plans?”

Hi kirti

I very much agree with your viewpoints.. Many people are unaware about the benefits of getting health insurance policy inspite of knowing that life is full of risks one can fall sick, get injure anytime anywhere and in all these situations health insurance policy helps overcome the medical expenses.. There are certain risks which people can feel before purchasing any policy. But for that there are various websites available now like http://www.policyx.com/ ,policy mantra from where people can easily compare and choose the best as per their requirements and be saved from fake commitments..

Hi kirti

I very much agree with your viewpoints.. Many people are unaware about the benefits of getting health insurance policy inspite of knowing that life is full of risks one can fall sick, get injure anytime anywhere and in all these situations health insurance policy helps overcome the medical expenses.. There are certain risks which people can feel before purchasing any policy. But for that there are various websites available now like http://www.policyx.com/ ,policy mantra from where people can easily compare and choose the best as per their requirements and be saved from fake commitments..

I agree with you Keerthi. We should keep away such things in mind that we are young and do not fall ill

Thanks Suresh. We know health insurance is needed but we don’t take it. But then we all know common sense it not that common

I agree with you Keerthi. We should keep away such things in mind that we are young and do not fall ill

Thanks Suresh. We know health insurance is needed but we don’t take it. But then we all know common sense it not that common