With home prices falling in six to eight major cities in the first quarter of 2021 and home loan interest rates now at a record low, there’s never been a better time to purchase a home in India, the Hindu reports. Buying a home is of course a major financial and emotional investment. It’s therefore important to be smart with your money and work to make your purchase as affordable as possible and in keeping with your financial goals.

Don’t forget these charges when buying a Home?

Table of Contents

What are the Charges while buying Home

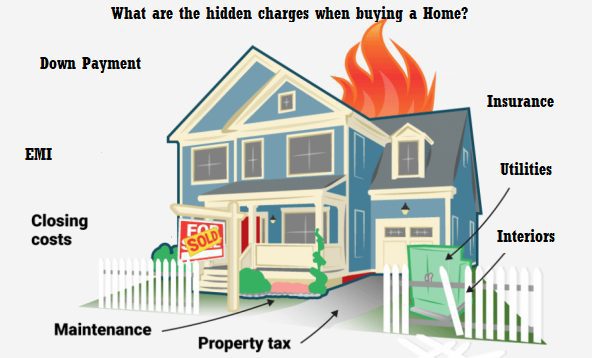

Buying a house is seen as a landmark moment in an individual’s journey. A first-time buyer usually focuses on the basic price, which is the rate per square foot. But there are many costs associated with purchasing a property. These go above and beyond just the price declared by the builder.

Additional charges can be on account of GST, maintenance charges, a deposit for electricity and water connection, registration and stamp duty, and so on. Since these charges come under other costs, banks generally don’t fund this.

If you buy a newly constructed home it would come without any furniture. You need to take account of interiors also.

There are apartments or gated communities with plenty of amenities to offer, like gyms, pools, basketball courts and more. It looked so glamourous and you could see yourself lounging by the pool, going to the gym. Would you have time to enjoy these amenities? And remember that these amenities would add to Maintaience charges.

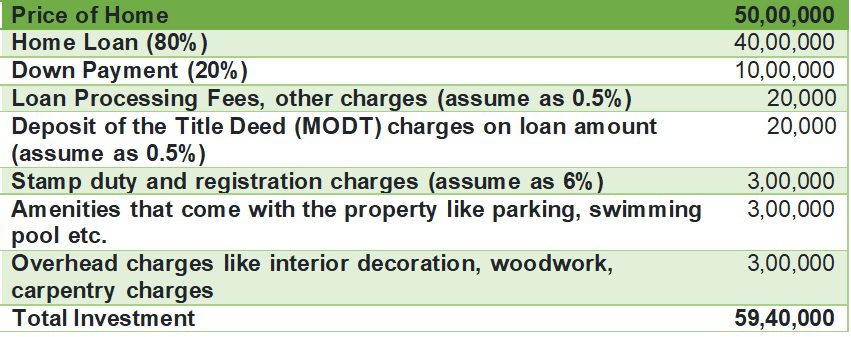

Calculating the extra charges of buying home

Aim to maximize your down payment

Saving up for a large down payment (at least 20% or more) has several financial benefits. For example, a larger down payment means you’ll get a lower mortgage rate as lenders use loan-to-value (LTV) ratio to measure risk and interest rates. A smaller down payment increases your LTV ratio, making your loan appear riskier to lenders, who’ll then charge higher interest to compensate. By putting more money down, you may be able to qualify for a better interest rate. Additionally, a large down payment also means you’ll have a smaller loan balance. This is beneficial as you’ll have more equity, which safeguards your home value even if market values go down. In turn, this can make the job of selling or refinancing your home much easier later down the line.

Choose an affordable mortgage

When it comes to home loans, it’s important to shop around and look at different options to find the best one for you, the Home Loan Expert explains. Mortgage rates and fees may differ from lender to lender, so getting estimates for the same loan from multiple lenders will ensure you find the most affordable option out there. Interest rates, APR, mortgage features, and settlement expenses are some of the main fees to contrast and compare. Moreover, if you can afford to invest in discount points, these can also work to decrease your interest rate. Discount points can be a useful purchase if you intend to live in your new home for many years.

Devise a prepayment plan

Prepaying your home loan means making early extra payments towards the principal of the loan — whether that means slightly increasing your regular monthly payment, paying a lump amount, or even doubling your monthly payment. By prepaying your home loan, you’ll be able to pay it off much faster as well as reduce the total amount of interest you pay. However, before starting to prepay your loan, it’s important to check if your lender allows you to do so without charging some type of penalty (many do). Additionally, you should ensure you’re able to make regular prepayments without putting yourself at risk of not being able to afford everyday and emergency bills and expenses.

Buying a home certainly doesn’t come cheap. However, by saving up for a larger down payment, choosing an affordable mortgage, and devising a prepayment plan, you’ll be able to purchase a home without breaking the bank.