Should School teach or talk about Money to Kids? Uma Shashikant, a personal finance writer thinks Financial planning skills are best learnt from parents, not at school. We are of opinion that Money should not be a taboo subject. It should be discussed at the school, at home, with friends like we discuss films, music, Netflix, holidays, birthdays. We conduct Money Sessions in school in Bangalore and we always come back impressed with how much the kids know and questions that they ask. But there is no escaping the fact that parents have a big influence on how kids look at money and decisions that they make and parents should have regular conversations, not lectures, with children about Money. This article covers Uma’s article, The Money session that we conduct in schools and How parents should have open dialogue with their children.

Table of Contents

Financial planning skills are best learnt from parents, not at school

Financial planning skills are best learnt from parents, not at school says Uma Shashikant. Uma Shashikant is Chairperson, Centre for Investment Education and Learning. Her articles appear in many newspapers and magazines. The article is given below. Reference: Economic Times

Including personal finance in school curricula is a favourite idea of many. They believe children should learn financial concepts at school to be better with money as adults. Despite being a teacher of finance, mostly to adults in the financial services profession, I find it difficult to advocate this view.

A school has its role in shaping the child, and the parents have theirs. While the child picks up language, math, science, arts and sports at school, apart from implicit skills of social behaviour, structure and authority, the life skills are quite in the domain of the household. Appreciating nature and the outdoors, eating a balanced meal, growing a garden, learning about one’s body, and understanding how to use money are skills, I believe, that parents have to teach. These skills are learnt from parents who impart it through their behaviour, through family activities and decisions that provide learning opportunities for the child.

The Money Advice Service, UK, in collaboration with Cambridge University, has been conducting several research projects about developing financial capability in children and young people. In the publication, ‘What drives financial behaviour?’ (April 2018), they provide a very useful framework. They classify the enablers and inhibitors of financial capability under three heads—ability, connection and mindset.

Ability refers to the knowledge of financial products and concepts about money and financial numeracy. Connection refers to engagement and access to money and money transactions. Mindset refers to values and attitude towards money, such as saving, confidence, understanding money’s value, and the financial position of the household. Unsurprisingly, the ability is not a driver of behaviour with respect to two key capabilities: day-to-day money management and active saving behaviour.

Teaching children financial concepts and products have no significant impact on how they managed their money or made simple decisions with money, or on whether they developed a saving habit. These key financial behaviours were influenced by the connection and mindset factors listed above. The responsibility for nurturing the right attitudes about money lies primarily with parents and not with the school.

What can parents do? The study shows that money habits are formed in children by the time they are seven years old. Children learn from several activities that help them connect with how money works in the household, and parents can enable this through active involvement and encouragement of children in making simple decisions. For example, a child who is handed over some money to go and buy a fruit for herself will find the experience of looking up the prices, making a choice, paying the money, counting the change, and enjoying the fruit a strong experience that enables connecting with day-to-day financial decision-making.

Knowing that money is a limited resource and that it comes from pursuing a job is an important learning for a young child, compared to the simplistic assumption that money comes from the ATM and swiping the credit card can buy anything. Children learn by observing how parents speak and behave. Ensuring that family conversations involve making joint money decisions, and involving children, are found to be valuable.

While planning a holiday, working with a broad budget and making decisions about how the money will be allocated to various heads enables children to understand opportunity costs. It also makes them feel informed and empowered about the decision the family makes on the holiday. To see that taking a bus instead of a taxi from the airport enables spending on extra scoops of delicious local ice creams provides the children with the capability to connect how considering alternate uses for money is important in managing it.

Attitude to a financial situation is developed from the decisions that the family makes and the experiences children have in participating in such decisions. Households that exhibit anxiety when the money runs short; households that are resigned to accepting that their money situation will not change; households that are wary about borrowing; and in contrast households that are nonchalant about borrowing are all implicitly imparting attitudes towards money in the minds of children. Confidence about managing money comes in when parents are able to actively demonstrate how to make difficult decisions with a limited resource.

The nightmare of a young child kicking and screaming in the toy section of a store is something most parents will identify with. It seems a tantrum ends up working in the child’s favour. Emotional intelligence and delaying of gratification are values taught primarily by parents, who make the conscious decision to do so. Psychologists conducted an experiment in which they told a group of young children that the primary purpose of one shopping trip was to buy a gift for a friend’s birthday. They handed over the budgeted money to the children, discussed the amount to be spent, considered the choices, and then allowed the children to walk through the aisles to make a choice. While children in the experiment were tempted by the toys they saw, they were reminded that the current purpose was not buying something for them, but for the friend. Advance notice that they won’t be getting anything for themselves, kept the children on track.

Values are tough to impart unless they are lived by the household and reinforced consistently over time. Children have an innate sense of fair play and learn by observing whether parents seek instant gratification or are able to wait and postpone a decision. Planned postponing of money decisions has been shown to have a strong influence on the mindset towards money.

Actually handling money, however small it is, and making choices have a lasting impact on building financial capability than the conceptual orientation towards making the child figure how a bank works. The Money Advice Service’s study showed about 40% of the variation in financial capabilities came from connections and mindset factors.

Older children understood financial concepts such as compounding quite well. Given a goal, many children took it upon themselves to earn, save and set aside money for a specific game, toy or gadget that they wanted to buy. They also understood deals, discounts and bargains.

Conceptual knowledge is mostly contextual. When a decision about taking a housing loan has to be made, understanding how the EMI is computed, how fixed and floating rates work, how a loan should be compared to income, are all important elements of financial literacy to know. Placing these in a school curriculum several years before that decision, may not achieve much.

School should talk about Money to Children

We are of opinion that Money should not be a taboo subject. It should be discussed at the school, at home, with friends like we discuss films, music, Netflix, trips. In school, we are taught so many subjects. In Schools Maths topics like Profit/Loss, Simple Interest/Compound Interest is taught in 7th-8th standard. But we are more concerned about solving the questions, getting the right answers rather than see how it impacts our daily life.

The way it is handled is different whereas school imparts and can impart general information about Money, it gives an opening for kids to talk about money.

Our Money sessions in School

We conduct money sessions in school.

In our 1 hour presentation with 1-page worksheet, We touch on following

Why is Money important?

Is Money Evil or Money is like a tool which can save a life or take life depending on whether it is in hand of a surgeon or murderer?

Do a role play on Shopping and tell them they have lots of choices and how discount work and why need to be a smart shopper

How do we pay for things bought – cash, credit card, wallets, cryptocurrency

Different ways in which people earn money – Talk to them about Robert Kiyosaki’s Employee, Self Employed, Business Owner and Investor.

Where do people keep the money? Talk about banks. Why bank pays interest to account holders?

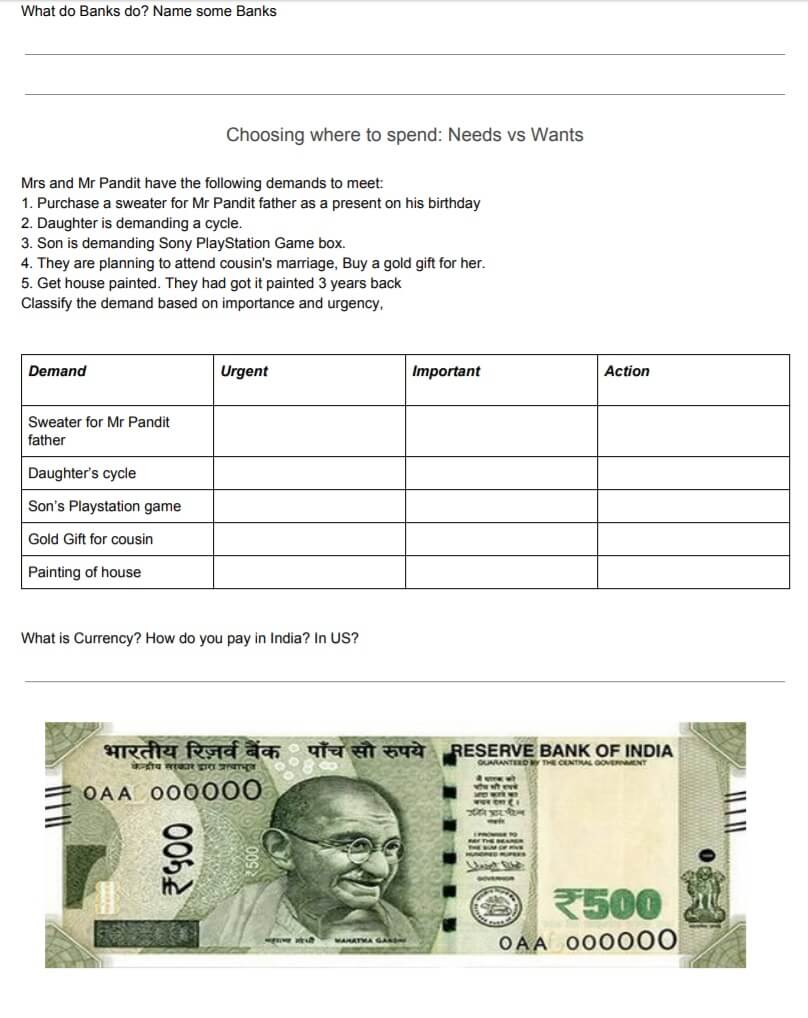

Discuss Indian Currency – Exploring the front and reverse of the notes, security features of the notes, why is rupee called rupee.

Talk about money of other countries. How Rupee is not only the name of the currency of India but of other countries like Nepal, Pakistan. How many different kinds of Dollars are there?

Talk about credit and debit cards.

Why paying the minimum on credit card leads to debt. When does compounding work against you?

We talk about how people visiting the Tirupati temple are still paying the debt of Balaji which he took from Kuber for his marriage.

We then talk about that Money in a family is limited and why we need to focus on Needs and Wants.

The Worksheet you can find it at the end of the article

How Parents should talk to Children about Money?

You Kids already know more than you think. Whether it’s the house you live in, the car you drive or the vacations you take, your children are surrounded by clues to family wealth but may lack the context to understand what that money really means.

Every parent’s goal is to raise a child who can thrive as an adult and dealing with money is one important aspect of adulthood. Overcoming the reluctance to talk about money is the first step on the road to helping your children form a healthy relationship with wealth. As a general rule, conversations are much more effective than lectures.

For instance, when you are at the ATM with kids, it’s a great opportunity to explain how you put money in the bank to keep it safe and to have money there when you need it, and that you can only take out as much as you put in.

Ask your kids questions that encourage them to formulate their own answers. For example, if your child asks you, “Are we rich?” your response might be, “That’s a really interesting question. You tell me; what does it mean to be rich?” And when they ask “How much money do you make?”, You should ask them “how much they think it is comfortable to have” And take this opportunity to talk about different jobs and how different skills are required to earn.

Talking with kids about money is an ongoing dialogue, not a one-time conversation. As your children grow conversations about wealth will evolve.

If a parent is looking for a workbook or the book on Money then they can try our book and workbook. Details can be found at Lets Learn About Money: Book

Let’s Learn about money Workbook The workbook worth Rs 50 is a pdf which will be mailed to you instantly after the purchase.

Mumbai Mirror Article on how parents talk to children about Money

From Mumbai Mirror Tried and tested parenting solutions on Aug 2018

“Money — the idea that something is cheap or expensive — can be a very abstract concept for children. I tackle this by letting them see, firsthand, how money is used as a medium of exchange,” says 27-year-old Mumbai resident, Charu Kataria.

Kataria takes her daughter to the market and shows her how a certain amount of money translates into the purchase of a certain amount of materials. “When my four-year-old daughter Amaira wants to buy something, instead of just saying yes, I always talk to her about why she needs that object. If it turns out that her desire for it is just impulsive, not driven by a specific need, I do not hesitate to say ‘no’,” she says.

Kataria also involves her daughter in basic discussions about say, the cost of groceries, when she makes a list of household expenses or works out the family budget. This helps Amaira to understand the importance of using money wisely.

Dr Bangar, who is the mother of a nine-year-old and a four-year-old, lets her sons ‘earn’ the things they really want. “The boys receive a small payment for every household chore they do. Once their savings have grown, they may buy the thing they were determined to. Not only does this teach them to plan, it also shows them that they must choose wisely when it comes to spending and gives them a sense of achievement,” says Dr Bangar.

Worksheets

One response to “Should School teach Children about Money?”

Really great article 🙂